United Steelworkers’ Insurance Fund (Highmark Blue Cross/ Blue Shield) plans were created to mirror FCE’s plans to give us a baseline for price. This is not a drastic change in price, as many of us hoped it would be, but the prescription plans have the ability to save all LDRM employees hundreds per year. We also have the ability to modify these plans an make them better, within costs that UE members feel is appropriate.

These are the initial quotes of the USW Insurance Fund’s BC/BS plans, we are reviewing a 5-tier system that separates the employee plus child and employee plus children plans.

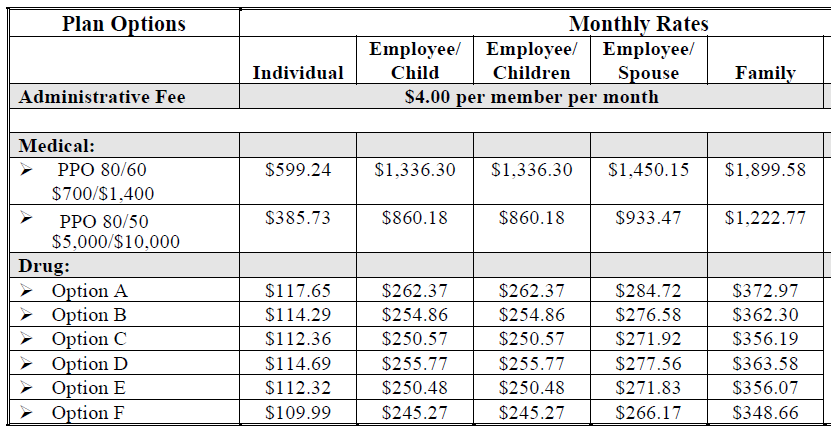

These are plans that LDRM does not want to make available to all of their employees (QHDHP price is in the plan documents). The links below contain comparison charts, along with plan documents. The premiums examples on the BC/BS 80/50 and 80/60 plans include the top tier prescription coverage.

FCE HSA v BC/BS Qualified High Deductible Health (Catastrophic Coverage)

For those who don’t plan on using their insurance unless absolutely necessary, pairs with an HSA. Everything, including prescriptions is 100% out of pocket until the deductible is met, then co-insurance kicks in

FCE Standard v BC/BS PPO 80/50 (Only covers after Deductible is paid)

Slightly better coverage than Catastrophic Coverage, out of pocket for services until deductible is met then co-insurance kicks in. Includes prescription co-pays (BC/BS plans offer six choices of prescription coverage)

FCE Plus v BC/BS PPO 80/60 (best coverage option)

Co-pays for Primary Care, Specialists, Emergency Room (FCE only), Urgent Care; Lower deductibles, lower out of pocket maximum

Any changes in the plans would be up to the members, so we would have the ability to say how much we are willing to spend for coverage, and what we want it to cover.

With that in mind, we have reached out to the plan to ask:

- Why the employee plus child(ren) plan costs more

- How much would the PPO 80/60 plan increase if we:

- decreased the $700 deductible to $500, $200, $0

- had copays instead of co-insurance

- reduced copay amounts

- Can the PPO 80/50 plan or the QHDHP plan be made less expensive (as these are the plans that people elect because of LDRM’s unnecessary group insurance requirement)

The outcome of 728’s arbitration (concerning waiving insurance) could raise the cost of our plans regardless of the carrier as a 10% change in the amount of covered individuals automatically causes a recalculation of rates, at the same time if LDRM is able to hire and retain an additional 75 or so employees between both facilities it would trigger a recalculation too.

Both locals will be heading to the bargaining table next year, 228 before the end of February (at or before open enrollment), and 728 before the end of October. This gives us the ability to negotiate what changes we need to offset things as appropriate.